As part of our contractor blog series, we break down the potential payroll tax obligations you have with independent contractors.

This blog covers key considerations but is not an exhaustive guide. If you’re unsure, please seek professional advice.

who regulates payroll tax?

NSW: Revenue NSW. Revenue NSW ensures compliance with the Payroll Tax Act 2007 and provides guidance and resources for businesses to manage payroll tax obligations.

QLD: Queensland Revenue Office [QRO]. QRO ensures compliance with the Payroll Tax Act 1971 and provides guidance and resources for businesses to manage payroll tax obligations.

Each state and territory in Australia has their own payroll tax legislation. Even if you only have one worker operating out of a state, you may have payroll tax obligations.

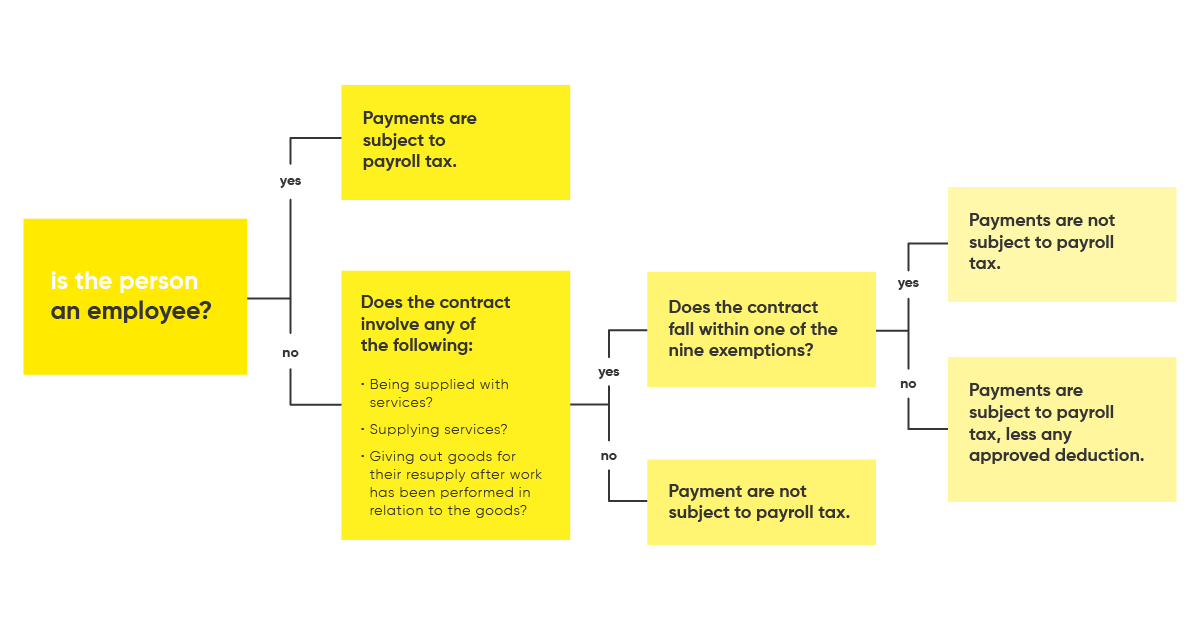

determining if a contractor is independent or a deemed employee

differences between employees + contractors

Employees work in and are part of your business for payroll tax purposes. They perform their work as representatives of your business, whereas contractors provide services to your business and perform work to further their own businesses.

Having an ABN does not automatically make someone a contractor.

Where a person is determined to be an employee, payments made to the person will be considered wages for Payroll Tax purposes.

NSW

Per Revenue NSW, a contractor will typically:

- be paid for hours worked, for results achieved, or for a combination of both

- provide materials, tools, and equipment necessary to complete the work

- be free to delegate work to other entities

- have substantial freedom in the way the work is done

- provide similar services to the general public, including other businesses

- be free to accept or refuse the work offered

- make a profit or loss

- incur significant costs of running a business, and

- bear the entrepreneurial risks associated with running a business.

If most of these factors don’t apply, the worker may be treated as an employee under common law and liable for payroll tax.

QLD

The Queensland Revenue Office provides a handy flowchart of things to consider to determine if payroll tax applies to a contractor or not.

Source: https://qro.qld.gov.au/payroll-tax/liability/contractor-payments/relevant-contracts/

A worker can be considered an ‘employee’ for payroll tax purposes even if they trade in a company, partnership or trust.

The QRO website states that “in most cases a contractor:

- is paid for results achieved

- provides all or most of the necessary materials and equipment to complete the work

- is free to delegate work to other entities

- has freedom in the way the work is done

- provides services to the general public and other businesses

- is free to accept or refuse work

- is in a position to make a profit or loss”

The website goes on to state that there are a number of factors to consider including;

- the right, authority or degree of control that the business operator can exercise over the worker

- how the contract describes the nature of the relationship compared to the actual relationship between the parties to the contract

- whether the focus is on the ultimate result or on what must be provided [e.g. labour]

- whether the worker is conducting their own business

- the capacity of the worker to pay others to undertake the services that the worker was engaged to provide

- whether the worker bears the commercial risk and responsibility

- whether the worker provides assets, tools and equipment or incurs overhead expenses

- indicators that suggest an employer-employee relationship, such as:

- the right to suspend or dismiss the worker

- the obligation to work

- working set and regular hours

- the payment of a regular or fixed remuneration

- the deduction of income tax

- providing superannuation benefits, annual leave, sick leave and long service leave

- requiring the worker to wear a company uniform.

As you can see the rules are very similar between NSW and QLD.

calculating taxable amount, if applicable

If your contractors are found to be deemed employees for payroll tax, typically only the payments made for labour services, excluding GST, are liable for payroll tax.

If the contractor supplied labour services as well as a non-labour component [such as equipment and materials], a deduction may apply. In such cases, the amount liable to payroll tax would be the total amount minus any GST paid and any non-labour component deduction.

payroll tax contractor exemptions

Revenue NSW has 7 contractor exemptions. If any of these exemptions apply, all payments made to that contractor are exempt from payroll tax.

The NSW exemptions are:

- Services ancillary to the supply of goods

- Services not ordinarily required by your business

- Services required for 180 days or less in a financial year

- Services provided for 90 days or less in a financial year

- Services provided by a contractor to the public during the financial year

- Services performed by 2 or more people

- Services provided by an owner driver

Some of the exemptions in QLD include:

- Services provided for no more than 90 days in a financial year

- Services required by your business for less than 180 days in a financial year

- Services performed by 2 or more people

- Services ancillary to the supply of goods

- Services not ordinarily required by your business

- Services approved by the Commissioner as exempt

- Services provided by an owner-driver

- Services relating to door-to-door sales

- Services relating to selling insurance.

example application of exemption Rules for Ally’s Allied Health Services Pty Ltd

As an example, we have applied the ATO guidance to a set of fictitious facts.

Please note that this is a NSW example, and the outcome may vary slightly in QLD or other states.

| Ally’s Allied Health Services Pty Ltd | Exemption | |

| Services ancillary to the supply of goods | Contractors primarily supply labour | Not exempt |

| Services not ordinarily required by your business | Services provided by the contractors are the key services offered by your business | Not exempt |

| Services required for 180 days or less in a financial year | To be reviewed on a case-by-case basis – nonconcurrent days | Undetermined |

| Services provided for 90 days or less in a financial year | To be reviewed on a case-by-case basis – based on concurrent days | Undetermined |

| Services provided by a contractor to the public during the financial year | No evidence of contractors advertising to the public | Not exempt |

| Services performed by 2 or more people | Only one person per contract provides services | Not exempt |

| Services provided by an owner driver | Not applicable | Not applicable |

Ally’s Allied Health Services Pty Ltd contractors are not exempt under five out of the seven exemptions. Some contractors may be exempt if they work fewer than 180 non-concurrent days or 90 concurrent days in a financial year; however, this would need to be assessed on an annual basis.

Co-authored by MD, John Knight.

you can review the other parts of our contractor blog series here:

we’re here to help

If you have any questions, please reach out to your usual contact at businessDEPOT. You can also give us a buzz on 1300BDEPOT or email us and our team will be happy to help.

get more insights

If you found this article helpful and you’d like to get more information, you can sign up to our mailing box here!